2023 – The year of H.O.P.E?

There is an acronym often used alongside talks of recession – HOPE. The acronym points to a sequence of data typically preceding an economic downturn. We usually see a fall in housing prices first, followed by declining orders and profits, and finally falling levels of employment. In this theme piece we look at some data that suggests that we may be half way through HO-PE already.

Throughout 2022 we have noticed market commentary flip flopping between positive and negative outlooks. The market has constantly battled to find direction with any certainty or consensus. Toward the end of 2022 we have observed some data in consumer activity that may point to where we are in the current cycle. Throughout the last two years of COVID disruption the usual signals and indices have been noisy and full of surprise, but we may now be seeing some clearer trends.

“Throughout the last two years of COVID disruption the usual signals and indices have been noisy and full of surprise, but we may now be seeing some clearer trends.”

We would firstly like to set some context by reviewing the economic environment in 2019 before COVID disrupted the world. In late 2018 the US Federal Reserve started raising rates. The Reserve Bank of Australia followed briefly also in late 2018. Consequently in 2019 consumer sentiment began falling as did Australian house prices. This resulted in a reversal and in mid-2019 the RBA began cutting rates. Total credit card balances had been decreasing through 2019 as people cancelled their credit cards, slowed spending, and started saving. Performance of Manufacturing Index (PMI) values fell and so did business profitability. Consumers had begun a slowdown and it had just started hitting profits before COVID emerged and disrupted

the cycle.

Housing

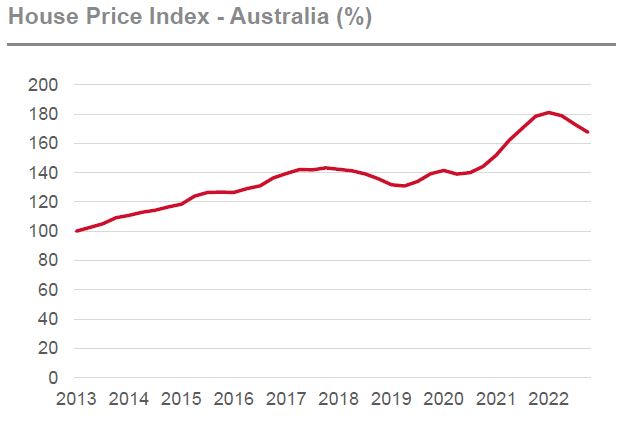

The HOPE acronym suggests that housing price falls are the first indication of potential recession. In Australia house prices, as measured by the Oxford Economics House Price Index, peaked in the early months of 2022 and by the latest data point at the end of November had fallen by nearly 10%. The Australian housing market experienced a surge through 2020 and 2021 driven by access to cheap capital, higher household disposable income (likely due to less discretionary spending) and the introduction of widespread remote working arrangements. The peak in housing prices has perfectly coincided with the Reserve Bank of Australia’s decision to lift rates rapidly from their historical low.

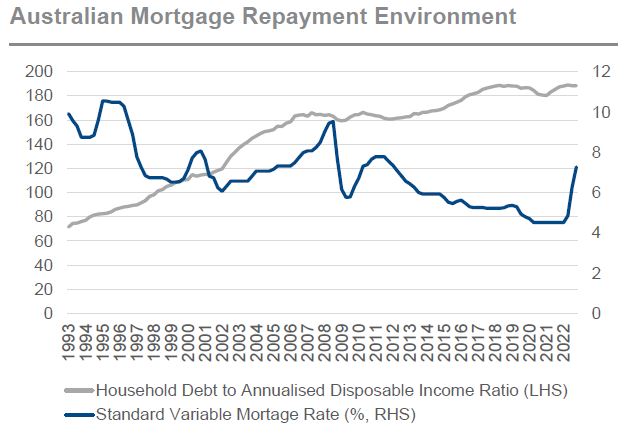

As you can see from the chart below, the variable mortgage rate has surged in a short space of time, but debt/disposable income ratios have not yet reversed. Various data and research we’ve seen indicates that a large portion of the Australian mortgage pool locked their mortgage rates during 2020/2021. Research from Credit Suisse has suggested that around one-third of fixed rate mortgages will reset to variable rates in the first half of 2023, another third in second half 2023 and the remainder during 2024. This will significantly increase monthly repayments for many mortgagees and have a significant flow on impact to spending.

Orders

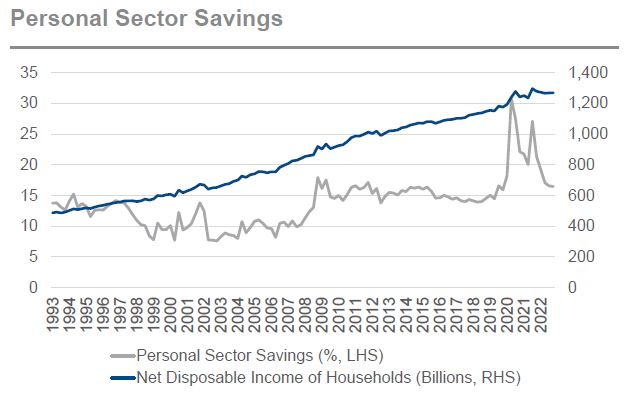

Consumer spending patterns have been a closely watched topic throughout the year and in recent months there has been a lot of commentary highlighting the resilience of consumer spending, particularly in the discretionary sector. Nearly 2 years of disrupted lifestyle and inability to travel freely has helped Australian savings accounts grow significantly. The personal savings ratio peaked in mid-2020 after months of restrictions and lockdowns hampered people’s ability to spend money on travel and entertainment. This accumulated savings quickly eroded between late 2020 and mid-2021 as restrictions eased and mobility increased. With the introduction of further restrictions for the Delta wave in mid-2021, savings balances climbed again although never quite reached their 2020 peak. Savings balances declined sharply around Christmas 2021 and have been falling throughout the year before stabilising around mid-2022.

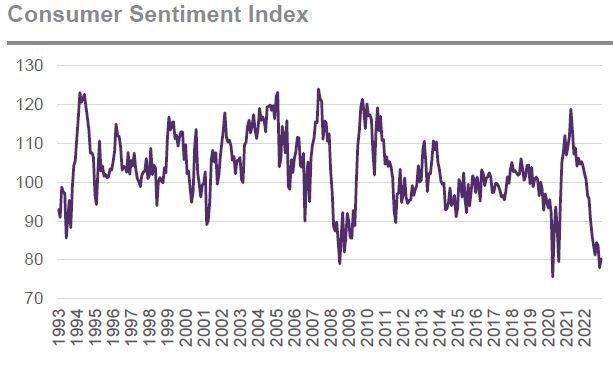

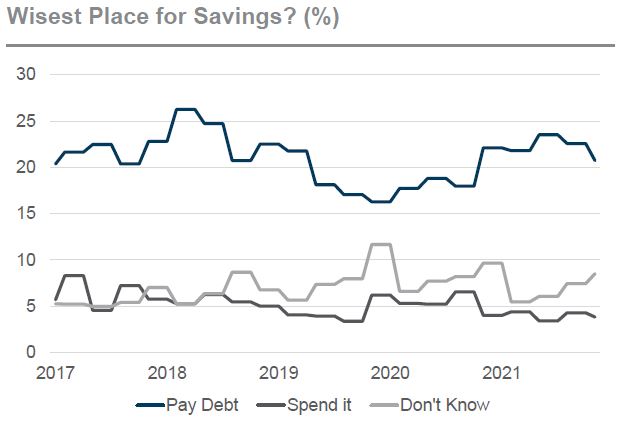

To analyse the orders component of HOPE we look to consumer data for some insight. We note that consumer sentiment, which is now at its lowest level in the last 30 years, has fallen sharply in line with declining savings balances. Since mid-2020, consumer surveys have shown an increasing portion of people allocating debt repayments as the wisest place for savings. At the same time people are becoming increasingly uncertain about where to allocate spare cash and less confident about spending it.

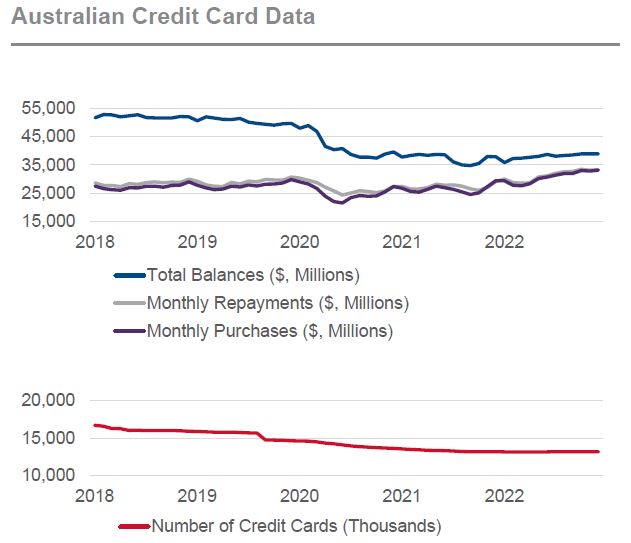

We find this interesting when compared to monthly credit card data provided by the Australian Bureau of Statistics. The number of credit cards in Australia began falling sharply in the second half of 2019 and continued falling throughout 2020 before stabilising later in 2021. We note that buy now pay later increasing in popularity in 2018 is likely to have partially contributed to this. After the Delta strain impact ended in late 2021 we saw a strong increase in monthly credit card spending with total credit card balances begin to climb again. Interestingly monthly credit card repayments have not grown at the same pace as purchases and cash advance transactions have risen, suggesting an increase in consumers’ debt burden.

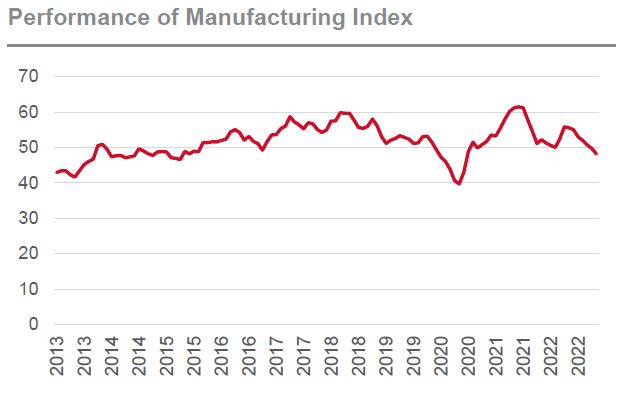

We are left with a scenario where savings ratios are back to 2019 levels, but interest rates are significantly higher, credit card debt has grown, the ratio of household debt to disposable income remains at all-time highs, cost inflation persists, all whilst real net disposable income has hit a plateau. Most mortgagees are yet to experience the interest rate rises affect their monthly repayments. Whilst spending hasn’t slowed yet, we’ve seen a sharp decline in Australian PMI data over the last few months. We think consumer spending data may show a decline in early 2023 particularly in the discretionary sector. This brings us to the next point – profits.

Profits

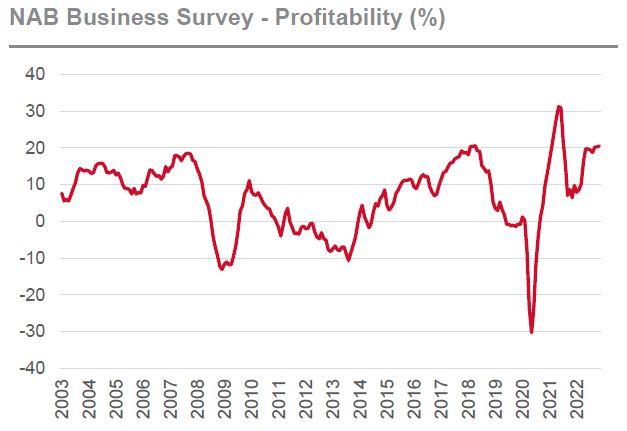

According to the Business Survey conducted by NAB, profitability is at its highest level since the first data point in 1997. It was only at the beginning of 2021 as the country emerged from lockdown with full savings accounts that business profitability was higher – and only slightly higher. Businesses were able to pass on cost increases to consumers because consumers were competing for limited stock and had the capacity to accept price increases. Now that supply chain issues have eased, freight costs are back at pre-COVID levels, and prices have remained elevated, businesses are enjoying elevated margins and profitability. Given the consumer data we’ve highlighted, we think profitability is likely to begin declining through 2023.

Employment

With persistent high inflation, there is increasing pressure

on employers to increase wages in line with inflation at a minimum. In the past this might have added 2-3% to wage costs, however currently this is likely nearly double the impact. With unemployment below 4% and many businesses still struggling to find staff, employment looks strong. However, travel restrictions for foreign workers have eased and the labour force is now increasing. This may provide businesses with a labour supply that may reduce labour inflation.

So, HOPE or Hope?

The recession of 2023 appears to be the most telegraphed recession of all time. The analysis above demonstrates from a well-worn historical perspective why this is the case. Using the HOPE analysis, we would appear to be well down the path of a few quarters of negative growth in 2023. However before concluding economically all is gloomy, we should perhaps remember another well-worn saying “No battle plan survives first contact with the enemy”. Inflation might surprise on the downside yielding central banks additional flexibility. Global travel may begin to reduce pressure on wages and labour supply. The Russia – Ukraine situation may head toward some form of armistice putting downward pressure on commodity prices and in particular the cost of energy. The risk of a property crisis in China declines combined with the achievement of COVID “normal”.

On balance, the Eiger team believe that the realignment of interest rates to positive real levels after two years of record levels of stimulus is likely to lead to tougher economic times. However, all is not bad. Economies and markets are dynamic and will respond to some events which will be positive for growth and inflation. Our job as investment managers is to find a sensible middle ground in these uncertain times. We want to own a select number of small-mid cap companies that provide us a good balance of some insulation from near term economic uncertainties combined with long term growth and value compounding opportunities.

This material has been prepared by Eiger Capital Pty Ltd ABN 72 631 838 607 AFSL 516 751 (Eiger). It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Any projections are based on assumptions which we believe are reasonable, but are subject to change and should not be relied upon. Past performance is not a reliable indicator of future performance. Neither any particular rate of return nor capital invested are guaranteed.