How does our process take advantage of early stage ideas?

In the past we have discussed our approach as small cap managers to position sizing and its importance given the large investable universe – about 700 companies between A$100m and A$3bn. Choosing a company to invest in goes beyond a purely quantitative approach and major considerations include liquidity, maturity of the business and the appropriate size within the portfolio. In other words, the highest alpha opportunity does not necessarily equate to the biggest holding.

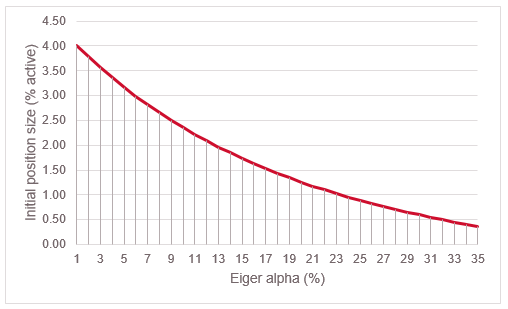

The chart below is a schematic illustration of this point. It shows the projected growth of a company’s holding size with a portfolio if our assumptions and modelling prove to be right. So, a company with a very high alpha, say 35%, could enter the portfolio at 50bps only and all other things being equal, could grow to about 4% without us adding to the position. If the company turns out to grow as we have assumed and we gain more confidence in the investment, then we might choose to add to it.

Source: Eiger Capital

We therefore do not need to take big risks on small, earlier stage opportunities. If we are right about the stock, growth will be very strong, and we should be rewarded with increased market capitalisation and share price. However, if we are wrong, the impact on the portfolio is limited.

Around 80% of our portfolios by stock number are anchored around more sizeable, liquid companies where we have a lot of confidence in the medium to long-term outlook. These companies are typically a bit more mature in their development but would also be considered as being higher quality (e.g. strong management, higher returns on capital etc) and still have prospects for efficient growth. The balance of the portfolio is a ‘nursery’ of ideas that we believe have excellent potential in the medium to long-term but are earlier in their journey.

One example where this investment approach has worked well for us is Pilbara Minerals (ASX: PLS), a WA based hard rock lithium miner. It’s a position held in the Eiger portfolio since fund inception in early 2019. As the saying goes Pilbara has been an overnight success some years in the making. Scoping the upside was never the issue. Our challenge was always managing the elevated risk in Pilbara’s earlier stage of development (high project capex and funding risk) and then forecasting the medium to long term demand for lithium battery grid storage and EVs.

In early 2019, our Pilbara alpha score (our DCF valuation models expected 6 year compound annual return) was well in excess of 30%. Nevertheless, as noted above, Eiger’s initial position sizing risk management process lead us to commit to only a 1% initial position in Pilbara.

Pilbara began construction of its plant in WA during the previous lithium boom in late 2016. As events would have it, the sector was then hit with a severe commodity price downturn during the new plant’s commissioning in 2019 and 2020. It was during these difficult times that we became very impressed with how prudently the company was managed. Others in the industry were less well managed during this downturn

Around mid-2020, as the lithium commodity price approached its nadir, our active portfolio position in Pilbara was still around 1%, (at a share price of 25c). Although we subsequently took up our pro-rata entitlements in the capital raise of early 2021 (to fund the acquisition of its insolvent lithium producing neighbour, Altura), we did not otherwise materially add to the position over this time.

Nevertheless, over the past 2 years, Pilbara Minerals has been the fund’s largest performance contributor, by some margin (Dec 21 share price of $3.20). This performance is despite our 5% “Hero Rule” (risk constraint of a max 5% active position) forcing us to continuous trim of our holding during 2021. At the end of 2021 Pilbara Minerals remained our third largest position, representing ~3.8% of the fund. It has delivered our investors over 9% alpha contribution over the past two years, all from that initial 1% position size.

A negative example involves Polynovo (ASX: PNV). We were very impressed with the NovoSorb technology that offered burns and wounds victims much better recoveries and outcomes. This product had a global total addressable market (TAM) of US$1bn but It was also developing similar products in areas with bigger addressable markets such as hernia treatment and breast reconstruction. Two years ago, we had a portfolio position of ~1% or an active position of about 65bps. This doubled over the next 12 months through share price appreciation to ~1.45% active. Unfortunately, several waves of COVID impacted the company’s US expansion and the CEO departed, so we chose to exit and wait for more stability in the business before reconsidering an investment. As Pilbara has shown, when small companies get things right, they can grow at an exceptional rate.

Today there continue to be several other small “nursery” positions of 1% or less in the fund. Examples include Calix (ASX: CXL), Eagle Mountain Mining (ASX: EM2), Boss Energy (ASX: BOE) and Chalice Mining (ASX: CHN). Calix has developed an innovative decarbonisation technology that has widespread potential in carbon-heavy industries, in particular the cement and steel industries, which combined account for about 15% of global carbon emissions.

Eagle Mountain is a brownfields copper company with a resource in Arizona, USA. It is aiming to expand the skarn copper resource and recommence mining. It is well-located in a major copper producing region, notable for some large porphyry deposits, and has had some exciting drill results from the skarn, possibly fed from a porphyry lode. It has also made a new gold discovery nearby at Golden Eagle.

Boss Energy gives us exposure to the uranium market, which has seen renewed interest since COP26 and the establishment of the Sprott Physical Uranium Trust. Boss is in South Australia, is fully permitted to produce and export uranium and requires only about 12 months to come off care and maintenance to begin production. The uranium sector has been capital starved for a decade and more focus on alternatives to fossil fuels has seen uranium prices increase dramatically over the past year from US$18/lb to US$42/lb.

Chalice Mining represents one of the most significant base metals and PGM discoveries in Australia in recent years. It recently announced a maiden resource of 330Mt @ 0.58% Ni eq at Julimar, WA (Gonneville) from about a quarter of its exploration holdings there. The company is now moving onto ground not previously explored and there remains strong potential for further positive results. We believe the suite of metals at Julimar (Ni, Cu, Pt, Pd) is attractive because of their widespread use in the renewables sector (in batteries, electrification and catalysts in hydrogen fuel cells).

There are also a small number of what were original sub 1% nursery positions over the past 2-3 years that have graduated into the top end of nursery holdings as they successfully prove out our investment thesis (now 1.5-2% active positions). Some examples include Audinate (the global leader in IP networked audio and video solutions), PWR (innovative thermal cooling technologies for automotive and increasingly defence industries) and PEXA (dominant Australian digital property exchange marketplace with opportunities to replicate similar position in other large property markets).

Most of these nursery positions have the potential to deliver our investors significant excess returns over the next 5 years plus. However, we are also realistic to accept that not all these ideas will work out as successfully as Pilbara. Nonetheless, we believe our measured risk-taking approach to these high alpha opportunities means not betting the farm on any single idea whilst providing our investors exposure to some of the better earlier stage opportunities in our investment universe.

This material has been prepared by Eiger Capital Pty Ltd (ABN 72 631 838 607 AFSL 516751) (Eiger) the investment manager of the Eiger Australian Small Companies Fund (Fund/s). Fidante Partners Limited ABN 94 002 835 592 AFSL 234668 (Fidante) is a member of the Challenger Limited group of companies (Challenger Group) and is the responsible entity of the Fund(s). Other than information which is identified as sourced from Fidante in relation to the Fund(s), Fidante is not responsible for the information in this material, including any statements of opinion. It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. You should consider, with a financial adviser, whether the information is suitable to your circumstances. The Fund’s Target Market Determination and Product Disclosure Statement (PDS) available at www.fidante.com should be considered before making a decision about whether to buy or hold units in the Fund(s). To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Past performance is not a reliable indicator of future performance. Any projections are based on assumptions which we believe are reasonable but are subject to change and should not be relied upon. Eiger and Fidante have entered into arrangements in connection with the distribution and administration of financial products to which this material relates. In connection with those arrangements, Eiger and Fidante may receive remuneration or other benefits in respect of financial services provided by the parties. Fidante is not an authorised deposit-taking institution (ADI) for the purpose of the Banking Act 1959 (Cth), and its obligations do not represent deposits or liabilities of an ADI in the Challenger Group (Challenger ADI) and no Challenger ADI provides a guarantee or otherwise provides assurance in respect of the obligations of Fidante. Investments in the Fund(s) are subject to investment risk, including possible delays in repayment and loss of income or principal invested. Accordingly, the performance, the repayment of capital or any particular rate of return on your investments are not guaranteed by any member of the Challenger Group.