Managing Risk in Small Caps

The standard industry method –Does it work well in small caps?

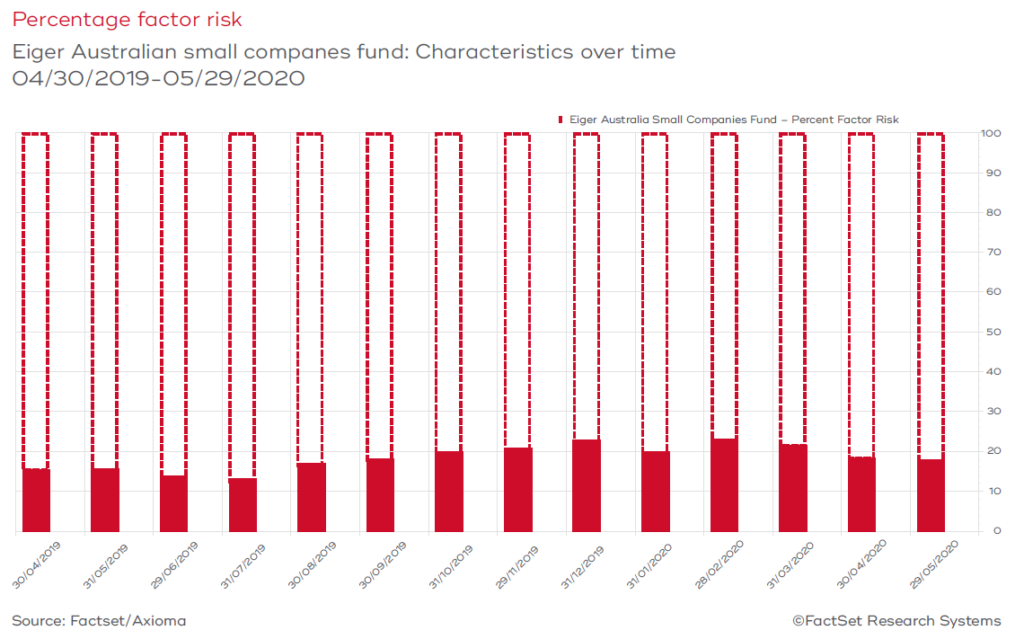

The standard method for dissecting risk exposure vs an index is the use of a commercial risk model, such as Axioma, that can accurately track variances in portfolio factors such as momentum, value, volatility, quality and size. Around 80% of the risk in a large cap portfolio, benchmarked against the S&P/ASX 100 Accumulation Index or S&P/ASX 200 Accumulation Index (ASX 200), can be measured and segmented using one of these models. The unexplained risk balance, typically around 20% in many large cap funds, is due to stock specific risk. However, for a concentrated small cap portfolio, such as the Eiger Australian Small Companies Fund, an industry standard risk model can only explain around 15% of the risk exposure vs the S&P/ASX Small Ordinaries Index (ASX Small Ords). The following chart highlights that between April 2019 and May 2020 the Axioma risk model we use can only explain between 12% and 22% of the risk in our portfolio vs the ASX Small Ords.

The balance, as in a typical large cap portfolio, is due to stock specific risk. However, in small cap

portfolio such as ours, stock specific risk is 80% of the risk vs the benchmark rather than 20%.

The volatility of our portfolio is higher than the ASX 200 but lower than the ASX Small Ords….

Does this make a portfolio such as ours excessively risky or volatile? We believe that the answer is definitely no. In addition, what this also highlights is that our portfolio of typically 30-40 stocks is not a portfolio that is constrained by a benchmark or any other overly restrictive factors that can inhibit performance. The Eiger Team has managed a small cap strategy continuously since April 2011. The standard deviation of daily returns (a universally accepted measure of volatility) of this strategy to the end of May 2020 is 1.019%*. The daily volatility of the ASX 200 and the ASX Small Ords over the same period was 0.99% and 1.054% respectively. Our portfolio over this time period has been less volatile than the ASX Small Ords Index and closer to the volatility of the ASX 200 that is dominated by Australia’s largest and most secure businesses such as the major banks, supermarkets and diversified mining giants.

We have also analysed longer term data from similar small cap funds published by Morningstar. For example, the UBS Australian Smaller Companies Fund between inception in March 2004 and November 2018 had a daily return standard deviation of 0.99%. The ASX 200 and ASX Small Ords had a daily standard deviation of 1.027% and 1.078% respectively over the same time period. We believe that it is possible to manage the overwhelming influence of stock specific risk in a concentrated small cap portfolio to take advantage of the high growth, innovation and entrepreneurial management and achieve a level of risk and volatility in line with the broader ASX 200.

Another way of analysing strategy volatility is to count the number of days the relevant fund’s unit price has varied above a specified amount. We have 4,123 days of observable unit price data for our small cap strategy. On 241 (5.8%) occasions the unit price has varied by more than 2%. Increasing the variance to 5% reduces the number of occasions to only 10 (0.2%). This is despite the strategy investing only in small – and mid-cap companies whose individual share prices are often much more volatile.

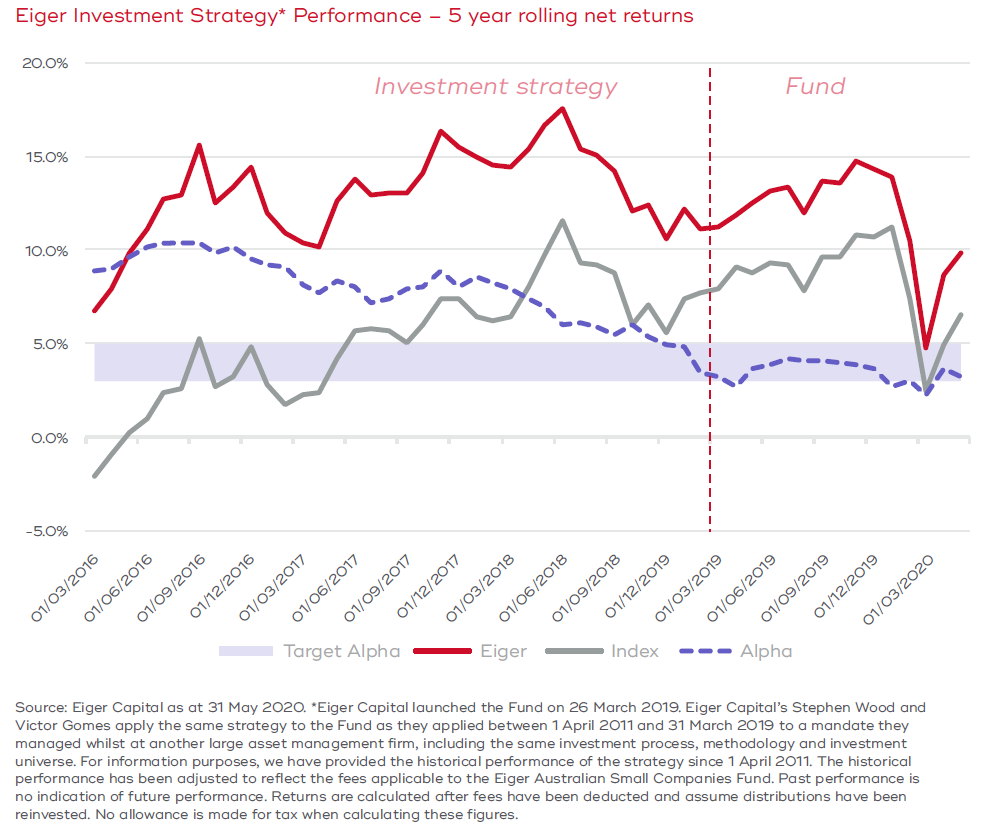

…but the historic returns are higher

The five year through-the-cycle track record of our small cap strategy is shown in the chart below. Despite having lower volatility than the ASX Small Ords the through-the-cycle returns have consistently been higher.

Managing stock specific risk

We have continually refined the way in which we manage stock specific risk, which as discussed typically accounts for around 80% of the total risk within our small cap strategy. We have measures in place to maintain a level of volatility below that of the ASX Small Ords, including:

1. Our research process requires us to construct our own models and forecasts rather than significantly rely on broker estimates, financial databases or consensus forecasts.

2. Our modelling template – which is largely unchanged for over 15 years – includes a significant quality bias with its focus on growth, operating cashflow and the consumption of cash via capex, working capital and intangible investment.

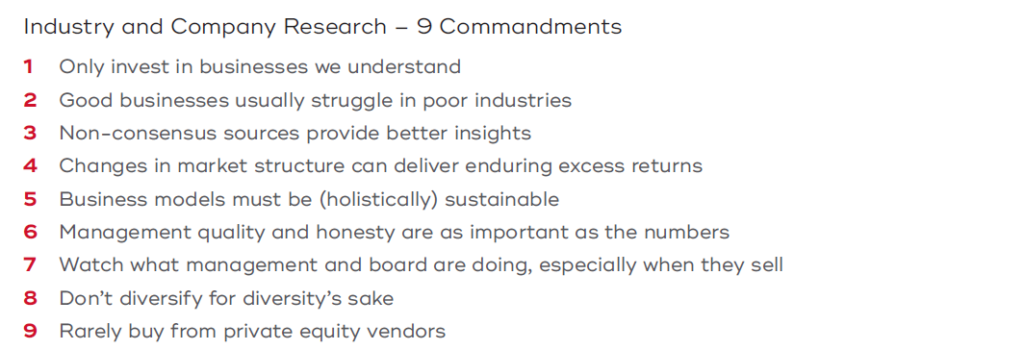

3. Our 9 Commandments which have been formulated over the 70+ years that our team collectively has in financial markets.

4. Portfolio constraints that include a 5% active limit on any one investment. We believe that this limit has worked time and time again in making sure that, for example, after a strong short term rise in a share price that some profits are harvested. As Bernard Baruch said over a hundred years ago “nobody ever lost money taking a profit”.

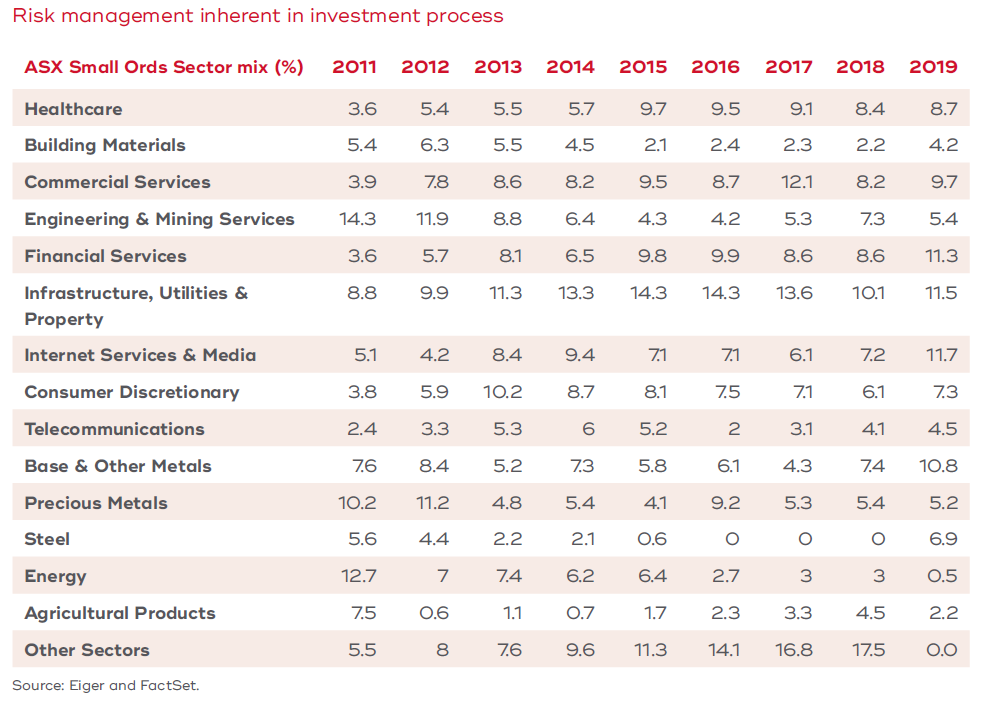

5. A proprietary fundamental reclassification of our investment universe into 25 categories. The following table charts the ASX Small Ords, which forms a significant portion of our investible universe, into these categories. We use these classifications to manage the fundamental underlying profit drivers within our portfolios. This ensures that we don’t accumulate excessively concentrated economic biases with our individual bottom up stock selections. We have continued to refine these categories for almost 10 years and believe they more fundamentally recognise economic risk than the standard Global Industry Classification Standard (GICS) classifications. The table below also highlights how significantly the sector bias has changed over time and the necessity to manage risk against these changes.

We believe that these factors are key to achieving risk and volatility well below the ASX Small Ords and more in-line with the ASX 200.

Disclaimer

1. Eiger Capital launched the Eiger Australian Small Companies Fund on 26 March 2019. Eiger Capital’s Stephen Wood and Victor Gomes apply the same strategy to the Fund as they applied between 1 April 2011 and 31 March 2019 to a mandate they managed whilst at another large asset management firm, including the same investment process, methodology and investment universe

This material has been prepared by Eiger Capital Pty Ltd ABN 72 631 838 607 AFSL 516 751 (Eiger), the investment manager of Eiger Australian Small Companies Fund (Fund). Fidante Partners Limited ABN 94 002 835 592 AFSL 234668 (Fidante) is a member of the Challenger Limited group of companies (Challenger Group) and is the responsible entity of the Fund(s). Other than information which is identified as sourced from Fidante in relation to the Fund, Fidante is not responsible for the information in this material, including any statements of opinion. It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. You should consider, with a financial adviser, whether the information is suitable to your circumstances. The Fund’s Target Market Determination and Product Disclosure Statement (PDS) available at www.fidante.com should be considered before making a decision about whether to buy or hold units in the Fund. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Past performance is not a reliable indicator of future performance. Any projections are based on assumptions which we believe are reasonable but are subject to change and should not be relied upon. Eiger and Fidante have entered into arrangements in connection with the distribution and administration of financial products to which this material relates. In connection with those arrangements, Eiger and Fidante may receive remuneration or other benefits in respect of financial services provided by the parties. Fidante is not an authorised deposit-taking institution (ADI) for the purpose of the Banking Act 1959 (Cth), and its obligations do not represent deposits or liabilities of an ADI in the Challenger Group (Challenger ADI) and no Challenger ADI provides a guarantee or otherwise provides assurance in respect of the obligations of Fidante. Investments in the Fund(s) are subject to investment risk, including possible delays in repayment and loss of income or principal invested. Accordingly, the performance, the repayment of capital or any particular rate of return on your investments are not guaranteed by any member of the Challenger Group.