Tailwinds in a Rapidly Evolving Defence Industry

Identifying next-generation defence opportunities

Faster procurement cycles have increased the quality of defence company earnings but require firms to be increasingly agile. We are prioritising investing in companies with strong track records of innovation, fast commercialisation, and new product development.

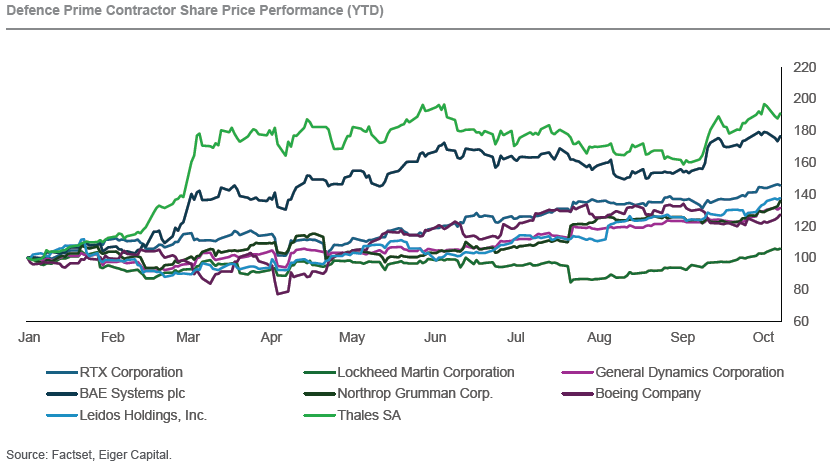

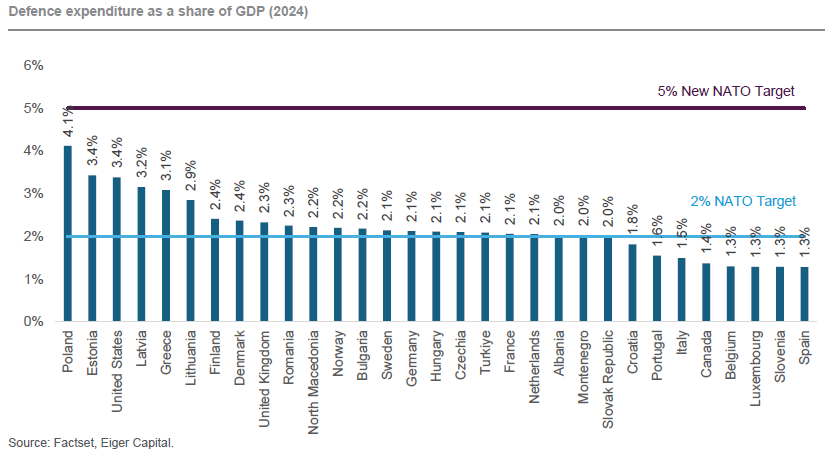

Heightened geopolitical risks have prompted the EU to be more receptive to aligning the global defence budget with US President Trump’s suggestion that NATO members lift defence spending from c.2% of GDP to 3.5%. The US leads the world in defence spending at 3.4% of GDP, which for decades has perpetuated their defence industry’s superiority. The US prime contractors are incumbents for defence contracts globally and often muscle out local defence hopefuls for contracts. Trump’s spending demands now come with a real consequence as the Ukrainian conflict is beginning to intrude on NATO member territory, reigniting focus on domestic defence spending. Since the beginning of the year these global defence primes are up on average 60%.

A shift in procurement

At the same time, operational lessons from the Ukraine war have highlighted a blind spot in the traditional approach of slow bureaucratic large-scale tenders. The need to counter drones requires low-cost solutions designed with collaboration, rapid iteration and deployment, and threatens the traditional deployment cycle. This has led to initiatives like the Brave1 marketplace, where military personnel can compare, purchase, and provide feedback on newly developed military equipment. This has provided an excellent opportunity for competing defence firms to prove up their technology in a demanding environment. Countries are also looking outside the US to grow their defence industries, a further tailwind to challengers. For example, Germany’s 2026 defence budget is expected to be over 80% supplied outside the US.

Lessons from PWR Holdings

Junior defence stocks have historically been challenging for investors; a small contractor with an edge on niche technology going up against an incumbent prime has struggled in the past. Only recently, investors have seen this dynamic with PWR Holdings’ (PWH-AU) entry into defence contracting. Despite their best-in-class cooling solutions business, powering many on the F1 grid, earnings from their Aerospace & Defence segment have been delayed and downsized. Segment revenues have grown from $4.6m in FY21 to $26.9m in FY25; however, sizable contract wins have been difficult, and delays once again led to downgrades at the August result. Among other things, the investment in overhead for this opportunity has assisted in a decline of their EBITDA margin from 36.6% in FY21 to 21.8% in FY25.

New competitors on the block

This enlivens the danger for investors, companies with enviable technology still finding it tough when operating in the Government / Defence prime market. We compare this to Electro Optic Systems (EOS) and Drone Shield (DRO). Electro Optic Systems boasts an ex-US lead over its peers in High Energy Laser Weapons, having signed the first commercial contract for development of a 100KW laser. Concurrently, its Remote Weapons Systems have also experienced a renaissance in demand to combat the increasing drone threat. The company has rocketed to $5 per share and now trades on 8.5x times next year’s sales. We estimate EOS must sell 425 RWS units or 6 HELWs per year to place the business on the same EV/EBITDA multiple as the average defence stock. While this may be achievable, investors are consistently reminded of delays in government contracting. Drone Shield has been similarly successful, developing RF drone detection and jamming technology. It has an additional commercial lens when compared to EOS’ predominant military use-case but recently missed out on being selected as the prime contractor for the Land 156 contract. This leaves the stock trading on a 20.5x times forward sales multiple.

A high quality stock

The approach we have taken at Eiger is to play the defence thematic through the under-the-radar Codan Ltd (CDA). The company has five trading divisions which broadly sell high frequency and software defined radio products, metal detection products, and public safety communication equipment. Metal detection EBITDA of $108.4m was up 21% in FY25, equating to a 47% return on assets. These returns contribute materially to the group’s capability to reinvest 10% of revenue into R&D. While 74% of the R&D budget is allocated to the higher growth communications division, metal detection has also seen a ramp up in new product development in recent years. Our recent tour of the R&D facility in South Australia underscored the high-quality work at Codan and their commitment to continuous new product development.

Codan’s defence exposure

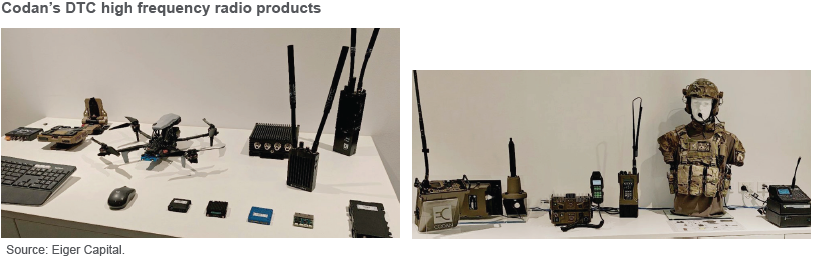

In the defence space, Codan sells metal detectors to armed forces and peacekeepers utilising its best-in-class detection capabilities developed since the 1960s. More recently they have branched out into software defined networks through the acquisition of Domo Tactical Communications in 2021. This technology has a range of use cases transmitting high fidelity communications data over a self-reinforcing network where access to public spectrum has been denied. This technology has been implemented in drones used in Ukraine through the collaborative and fast paced development cycle we touched on earlier. Revenue is growing strongly and importantly it is highly diversified by product and customer, taking the form of high frequency repeat orders. This differentiates Codan’s earnings quality in comparison to peers. At the site tour we saw firsthand how feedback was received from soldiers, steering the development of pack-mounted high frequency radios. Management have been strong stewards of capital; delivering an organic EBITDA growth CAGR of 36% since 2021 from its 7 communications acquisitions. That is effectively a doubling of earnings from businesses they collectively paid sub 6x EBITDA for. A great result.

Codan was one of our strongest performers in August, raising its revenue guidance for the communications to 15-20% growth, coupled with continued operating leverage. At the end of August, CDA was trading on 21x times forward EBITDA, despite being up 88% this year. This is in line with Motorola Solutions’ (MSI-US) recent takeover of competitor Silvus Technologies for 21x. Codan has a 25% ROIC and a solid balance sheet that it can continue to deploy in the defence sector, capitalising on its new product development and commercialisation engine. We see heightened opportunity in the sector from the competitive opening created by the Ukraine war but take caution that expectations are now very high and the sector has disappointed in the past.

Author: Sam Cox, Analyst

This material has been prepared by Eiger Capital Limited ABN 72 631 838 607 AFSL 516 751 (Eiger Capital). It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Any projections are based on assumptions which we believe are reasonable but are subject to change and should not be relied upon. Past performance is not a reliable indicator of future performance. Neither any particular rate of return nor capital invested are guaranteed.