There’s no such thing as a free (delivered) lunch!

If you hadn’t used a food delivery service prior to COVID, chances are that at some point during lockdown you tried it for the first time. If food delivery isn’t something you’ve used, then maybe you’ve booked an Uber instead of a taxi or used Airtasker to have something designed, couriered, or assembled. Food delivery services like Uber Eats, Deliveroo and Menulog experienced huge uptake during the various lockdowns and an already growing gig-economy continued to expand. You may have noticed more delivery bike riders on the roads than cars at some point – clear indication of the popularity of these services.

Companies like Uber have enjoyed a free ride with equity markets funding persistent losses and allowing consumers to have heavily subsidised rides and deliveries. These companies have also enjoyed lax regulation around their workforce management allowing them to avoid having drivers and riders classified as employees and therefore reducing insurance, wage, and superannuation costs. With governments beginning to push for unionising gig-economy workforces and thereby raising labour costs, increasing interest rates, and significantly lower equity prices, we see expenses climbing significantly and funding becoming far more expensive. The path to profitability for these companies is getting much harder and levelling the playing field with local companies like Dominos and KFC (Collin’s foods).

“Companies like Uber have enjoyed a freeride with equity markets funding persistent losses and allowing consumers to have heavily subsidised rides and deliveries.”

Indexed Price Change % (0 at 31 Dec 2020)

These gig-economy businesses have a commonality amongst them – their funding model. A persistently loss-making business must access capital regularly to stay operating as it attempts to generate a profit. For companies with a business model that is heavily dependent on providing a cost competitive service it is imperative to keep costs low. For many of these companies this means accessing cheap (we’d suggest almost free) capital. These companies have enjoyed a paradise of systemic market change (i.e. lockdowns driving the utility of these services) for nearly two years and at the same time have had access to near zero cost capital. Despite all time low rates, many of these companies have funded their loss-making business through equity raisings.

Uber, for example, generated around $40bn US of revenue during 2019,20,21. Over those three years it made a net profit (loss) of around -$17bn and raised ~$12bn primarily through equity issues. It is currently left with ~$5bn in cash and broker estimates suggest Uber will face a ~$9bn loss for 2022. Uber is now faced with financing 2022’s loss by issuing debt at much higher rates than it has previously or via equity raising at a share price that is half of it 2021 highs. As it does this, its hurdle to profitability becomes even higher and its investor base even more eager for the company to generate a profit. With the US target rate having risen from 0.25% (set March 2020 and held until March 2022) to 3.25%, and most other countries having similar rate raises, these companies face significant changes to the debt portion of their funding models.

“Given their low-cost funding has nowdried up, the response is likely to be raised prices for the services to cancel out the funding costs.”

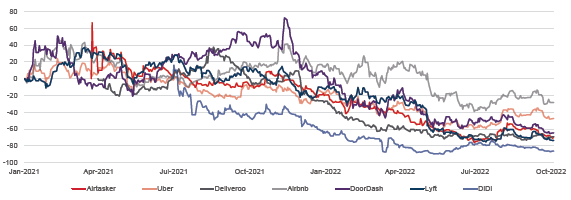

We looked at indexed share prices for Uber, Deliveroo, Airbnb, Airtasker, Doordash etc. and all of them have fallen at least 50% since the start of 2021 when they were during a low rate, high demand environment. Given their low-cost funding has now dried up, the response is likely to be raised prices for the services to cancel out the funding costs.

Not only has funding these losses become significantly more expensive, but there is also increasing pressure from Governments to regulate the gig-economy, particularly the labour agreement component. This change will create more complexity and operating risk for these companies as well as significantly increase their cost of doing business. In Australia, riders and drivers for these companies have been treated as contractors, not employees.

This has allowed companies to avoid providing equipment, insurance, stable salary with superannuation, and other employee benefits. Consider that some Australian delivery riders generate as little as $10/hr after costs (an E-bike or scooter is a significant expense for these delivery riders) and that the likely wage for this sort of occupation should be upward of $20/hr you can see that there is a significant cost impact of companies having their ‘contractors’ reclassified as employees. Add in superannuation and insurance that companies will have to start providing and the prospect of profitability looks far less likely without price rises.

We will be watching with interest as gig-economy stocks grapple with the prospect of price rises to reduce losses. This will also have an impact on their competitive positioning against the likes of the local listed Dominos and Collins Foods.

Source: https://www.afr.com/work-and-careers/workplace/deliveroo-overturns-ruling-rider-an-employee-20220817-p5balm

Disclaimer

This material has been prepared by Eiger Capital Pty Ltd ABN 72 631 838 607 AFSL 516 751 (Eiger). It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Any projections are based on assumptions which we believe are reasonable, but are subject to change and should not be relied upon. Past performance is not a reliable indicator of future performance. Neither any particular rate of return nor capital invested are guaranteed.